A category can look healthy on every dashboard you have. Four suppliers under contract, full participation on the last RFQ, nothing flagged in the latest spend review. And yet, quarter after quarter, the price keeps drifting in the wrong direction: flat when raw material indices say it should be falling, or creeping up when nothing in the contract justifies it. The dashboards are not wrong. They are simply measuring the wrong thing.

Most procurement reporting tracks presence: the number of suppliers consulted, the response rate, the size of the panel. It rarely tracks pressure: whether those suppliers are still genuinely fighting for the business, or have settled into an informal rotation where everyone keeps a comfortable share and nobody pushes too hard. A category can carry four active suppliers and almost no competitive tension at the same time. The two are not the same thing, and the gap between them is exactly where margin disappears without a single visible mistake being made.

That is the uncomfortable starting point. Declining competitive tension is rarely the result of a bad decision. It is the result of no decision at all, repeated across enough sourcing cycles that nobody remembers when the pressure was last real.

Why Competitive Tension Erodes Long Before Any Procurement Dashboard Notices

Why Supplier Count Is the Wrong Metric for Competitive Tension

Supplier count is the easiest number to report and the least informative one to act on. A panel of four suppliers tells you that four companies are willing to send a quote. It tells you nothing about whether those four still treat each negotiation as a contest they could lose. Markets with formally large panels routinely produce weaker pricing outcomes than markets with three suppliers who genuinely believe the business is at stake, because the second group is competing and the first group is participating.

This distinction matters because procurement organizations are structurally biased toward measuring what is easy to count. Panel size, RFQ response rate, number of bids received: these are visible, auditable, easy to put in a quarterly business review. Real competitive intensity, by contrast, only shows up in the shape of the offers themselves, and almost nobody is looking there systematically.

How a Procurement Category Quietly Loses Competitive Tension

The drift is gradual and, taken one cycle at a time, defensible. A supplier wins three consecutive renewals on a category and becomes the reasonable default for the fourth. A category manager, under time pressure, sends the RFQ to the same shortlist that worked last year, because qualifying new suppliers takes weeks the timeline does not have. This is not a failure of rigor on the buyer's part. It is the outcome of a human trade-off between chasing a competitive tension that might not materialize and the more immediate need to secure supply before the week is over. Suppliers, observing that the award pattern has been stable for several cycles, start pricing to protect the relationship rather than to win the deal outright, because the expected value of an aggressive bid that disrupts the rotation is lower than the expected value of a moderate bid that preserves their share.

The Two Negotiation Signals That Reveal Real Competitive Tension

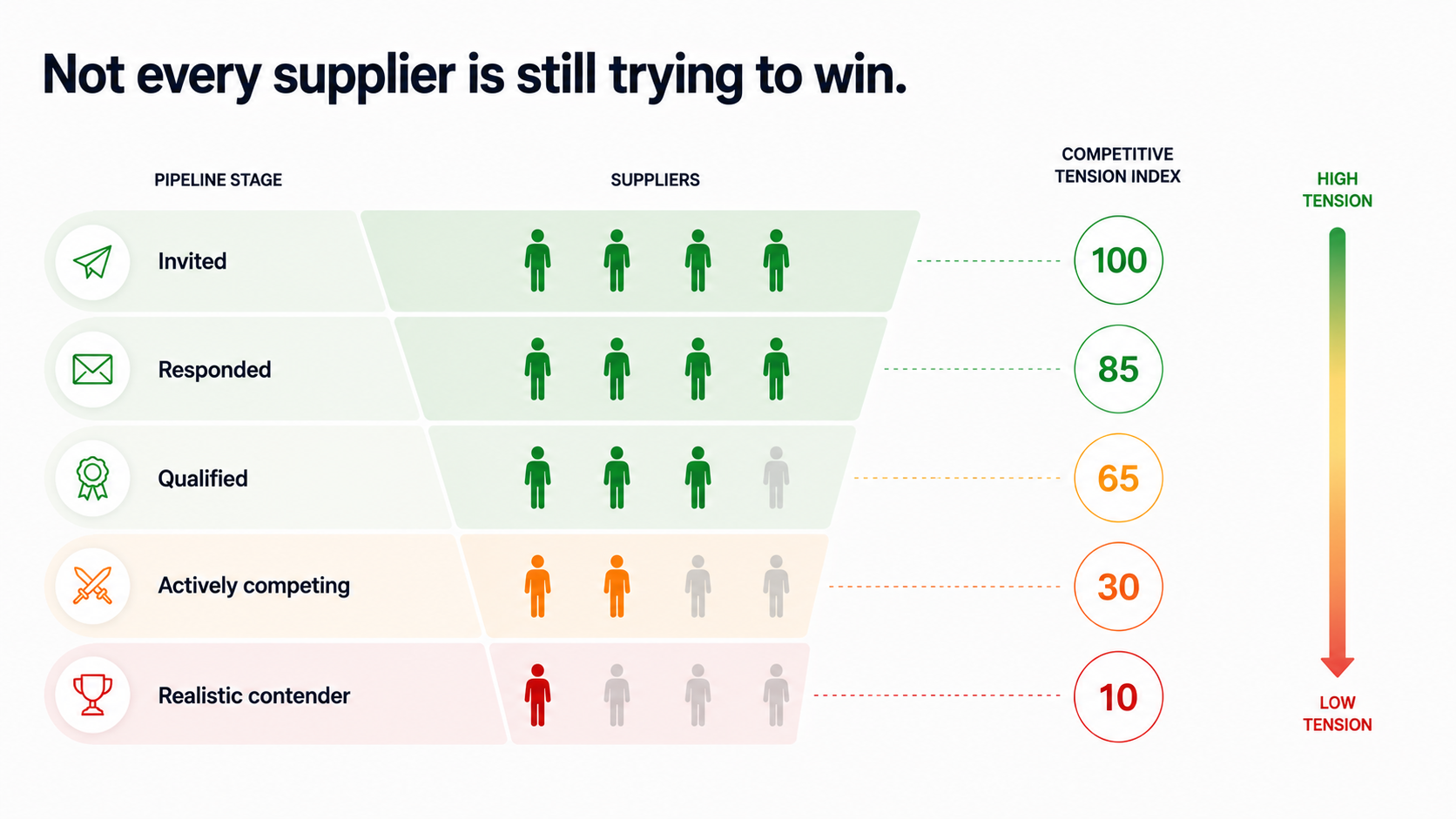

If supplier count is the wrong metric, two other numbers are far more diagnostic, and neither requires new tooling to track. The first is the number of suppliers genuinely active in the final stage of a negotiation: not invited, not consulted, but still bidding when the process closes. The second, and the more revealing of the two, is the spread between your two best offers. A wide spread, generally above ten percent, signals that at least one supplier still believes there is real ground to gain by undercutting the rest. A narrow spread, particularly when it has been narrowing for several cycles in a row, is one of the clearest early indicators that the panel has stopped competing on price and started competing on relationship maintenance.

Procurement teams that take this seriously build it into their sourcing diagnostics as a standard question, not an afterthought: how many suppliers are realistically in contention, and how far apart are their best offers. The answer to those two questions, tracked over time and by category, says more about where margin is leaking than any supplier scorecard built around delivery performance or service levels.

How a Change in Supplier Awarding Logic Can Close a Competitive Pricing Gap

The mechanism behind this erosion is well documented in negotiation practice, and one case illustrates it with unusual clarity. A procurement team running a recurring negotiation across several quarters had built up a real pricing advantage over the broader market by concentrating more volume on its most competitive supplier each cycle. The market price stayed flat. The negotiated price kept falling. A gap opened up and held.

Then the team changed the awarding principle, reverting to an equal split across all suppliers to keep a lagging incumbent motivated to stay in the race. Market conditions did not change. The number of suppliers did not change. Only the rule governing who actually wins changed. The result was immediate: the negotiated price jumped back up, and the competitive gap the team had spent several quarters building closed almost entirely in a single cycle.

The lesson is structural, not anecdotal. Competitive tension is not a property of the market or the supplier panel. It is a property of the mechanism you design around them. Change the mechanism without realizing it, and the tension you assumed was permanent evaporates immediately, with the price following a quarter later.

Kraljic Matrix Segmentation: Reading Category Risk Before You React

Not every category showing declining tension deserves the same response, and treating them identically is its own mistake. In leverage categories, where spend is concentrated and supply risk is low, declining tension is almost always a process failure waiting to be corrected: re-opening the panel, redesigning the award logic, or running a structured competitive event will typically recover the gap within a single cycle. In non-critical categories, the more efficient response is standardization and consolidation rather than renewed negotiation intensity, since the absolute value at stake rarely justifies the effort.

Strategic categories and bottleneck categories belong to a different conversation. Here, supply risk, technical dependency, or a genuinely small supplier base can mean that declining price tension is the rational price of stability, and forcing aggressive competition risks damaging continuity of supply for a saving that does not offset the exposure. The discipline is not to apply a single playbook everywhere. It is to know, category by category, where competitive pressure can and should be rebuilt, and where the right response is closer supplier management rather than a sharper negotiation mechanism.

What Safran and Other Disciplined Industrial Buyers Do Differently With eAuctions

The procurement organizations that catch this early share a common trait: they treat the negotiation mechanism itself as a variable to manage, not a fixed step at the end of sourcing. Safran's procurement teams, working on technical categories where supplier qualification is far from trivial, have used structured, time-bound competitive events on lots that still looked stable on paper, and recovered measurable savings in a matter of weeks rather than the quarters a renegotiation cycle would normally take. The point is not the speed for its own sake. It is that the structure of the event itself, transparent rules, real-time visibility into where each supplier stands, a clear closing point, reintroduces the contest that an informal RFQ rotation had quietly removed.

This is consistent with what disciplined buyers in heavy industry have understood for longer than procurement technology has existed: competitive tension is not something you wait for the market to provide. It is something you engineer into the process, deliberately, on a cycle that does not wait for the contract renewal date to arrive.

From Detection to Execution: Rebuilding Competitive Tension Before It Costs You the Quarter

Why Traditional RFQ and ERP eSourcing Cycles Arrive Too Late to Save Margin

A standard RFQ-to-award cycle, run through email or a generic sourcing tool, typically takes weeks to assemble, distribute, clarify, and compare. By the time the comparison is ready, the moment where competitive pressure could have been deliberately engineered into the process has usually passed, replaced by a negotiation that is really just a final round of clarifying questions before the expected supplier confirms the expected price. Large procure-to-pay platforms compound the problem rather than solving it: their AI-driven sourcing modules are typically built for long, IT-dependent rollouts, with results that arrive months after the category manager needed them. Where the eSourcing modules inside large ERP suites require weeks of configuration for every single event, competitive tension demands the opposite: tactical responsiveness, not a project plan.

What detects and corrects declining tension in time is a mechanism that compresses the negotiation itself into a single, structured, time-bound event, rather than a sequence of emails spread across several weeks. The diagnostic and the correction become the same motion: running the event surfaces, immediately and unambiguously, whether the panel is still competing or merely participating.

Why Mechanism Fairness Is the Only Guarantee of a Supplier's Best Offer

It is worth stating plainly that rebuilding competitive tension is not an exercise in pressuring suppliers into compliance. The procurement organizations that get the best results are the ones whose suppliers understand the rules in advance: clear evaluation criteria, visible award logic, and a process that treats every participant equally regardless of incumbency. Suppliers who understand exactly how they are being evaluated submit better offers, not because they are forced to, but because uncertainty about the rules is itself a source of conservative, defensive bidding. A transparent process reduces supplier frustration and consistently improves the quality of the responses procurement receives, which is precisely why the strongest sourcing organizations treat clarity toward suppliers as a competitive advantage rather than a courtesy extended to them.

What Changes When an eAuction Mechanism Generates Real-Time Competitive Pressure

Once the negotiation event itself becomes the source of pressure, rather than a formality that follows a negotiation already effectively concluded by email, the diagnostic problem this article opened with mostly resolves itself. You no longer need to infer, months later, whether a category has gone quiet. You see it directly, in real time, in whether bids keep moving as the event approaches its close, or stop the moment the usual supplier reasserts the expected position.

Procurement is moving toward a model where the negotiation mechanism is treated with the same rigor as the sourcing strategy that precedes it, rather than as an administrative step that happens after the real thinking is done. The categories that will hold their margin over the next several cycles are not necessarily the ones with the largest supplier panels. They are the ones where someone deliberately checks, cycle after cycle, whether the contest is still real, and rebuilds it the moment it stops being one. That is a discipline, not a tool, and it is one most procurement organizations have not yet built into their operating rhythm.

This is where infrastructure built specifically to compress and re-engineer the negotiation cycle, rather than to automate the paperwork around it, becomes the logical next step rather than an optional upgrade. CROWN exists for exactly this layer of the process: the moment where a category's competitive tension needs to be measured, rebuilt, and proven, not assumed.

If a handful of your categories have not seen genuine price competition in more than two cycles, that risk is already there. CROWN helps you analyze the real spread behind your latest offers and re-engage the market within weeks, without changing the tools you already have in place.